October marks ten years since the advent of automatic enrolment for workplace pensions. What’s been learned in the last decade?

The automatic enrolment (AE) of employees and other workers into workplace pensions faced scepticism when its initial phasing in began in October 2012. Plenty of pension experts had witnessed the failure of earlier initiatives to increase take up of pension saving.

This time the outcome was dramatically different, with participation rising from around 47% in 2012 to 79% in 2021. Much of that is due to its design:

- Inertia plays a major role – membership is automatic, so deliberate personal action is required to opt out.

- Employer and employee contributions were initially low before increasing in two stages.

- The first schemes were set up by the largest employers, who were best equipped to organise the roll out.

- The default provider, the National Employment Savings Trust (NEST), is at arm’s length from the government; it now has over 11 million members.

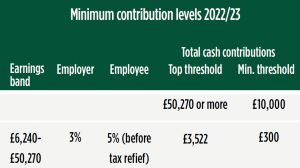

Contribution levels

The chances are that if your employer provides you with a pension, it is an auto-enrolled workplace pension. However, the success of automatic enrolment does not mean the issue of adequate retirement funding has been solved, either for you personally or the general workforce:

- The minimum level of contributions is still widely considered to be too low. The Association of British Insurers (ABI) recently suggested that to be adequate, employer and employee should pay 6% each, phased over the next ten years.

- As the table shows, no contributions are levied on the first £6,240 of earnings. This has a disproportionate impact on low earners. Without that restriction, contributions for someone earning £10,000 would be £500 more.

- Each employment is considered separately, which means people with more than one job who earn more than £10,000 in total receive no employer pension contributions at all. If the £6,240 exclusion were removed, then the current earnings trigger of £10,000 would also disappear.

Despite auto enrolment’s success, issues remain. The Association of British Insurers has suggested contributions should rise to 6% each for employer and employee.

The current system also overlooks the self-employed, who represent about one in eight of the UK workforce. While some gig workers have become eligible for AE pensions following Employment Tribunal decisions, the self-employed generally are left to their own retirement planning devices. As a result, currently only 16% of self-employed workers now save in a private pension, down from 50% 20 years ago.

In the current economic environment, no government is likely to risk proposing an increase in the mandatory minimum contributions, so taking action yourself may be more prudent. To find out if your current level of pension contributions, whether automatic or otherwise, are sufficient to meet your retirement goals, please get in touch.

The Financial Conduct Authority does not regulate tax advice. Tax treatment varies according to individual circumstances and is subject to change.

The value of your investment and the income from it can fall as well as rise. You may get back less than you invested.

Past performance is not a reliable indicator of future performance.